EOY! It's time!

- MenschSGP

- Nov 7, 2017

- 5 min read

It’s EOY again!!!

EOY : end of year

Each time when this season of the year comes around, there are a lot of activities going on.

Activities such as planning for the year-end winter (or summer) holidays, planning dozens of gatherings with friends and relatives in light of the festive (Christmas) season and a lot of shopping as retailers bring on their massive year-end sales!

Spend, spend, spend!!!

And that is what every individual will be doing!!!

Shining another light at you; how great will it be if you can create some savings for yourself during this period of time?

Amidst the retailers having their red hot promotions, there is a certain activity that is buzzing elsewhere and as of December 2016, only 127,753* have done so.

Is that a huge number out of the 3.87** million residents (SC and SPRs)? No.

So what is this activity that we are discussing about here?

It is the Supplementary Retirement Scheme (SRS) contribution!!!

“The SRS is part of the Singapore government’s multi-pronged strategy to address the financial needs of a greying population by helping Singaporeans to save more for their old age. It began in 2001 and is operated by the private sector. The SRS complements the Central Provident Fund (CPF). CPF savings are meant to provide for housing and medical needs and for basic living needs after retirement. Unlike the CPF scheme, participation in SRS is voluntary. SRS members can contribute a varying amount to SRS (subject to a cap) at their own discretion. The contributions may be used to purchase various investment instruments.”

- Source: MOF

So, why should you do it?

The SRS offers attractive tax benefits. Contributions to SRS are eligible for tax relief. SRS contributions made on or after 1 Jan 2017 are subject to a cap on personal income tax relief of $80,000 per Year of Assessment from Year of Assessment 2018.

Investment returns are accumulated tax-free and only 50% of the withdrawals from SRS are taxable at retirement (referred to as a “50% tax concession”). Please refer to IRAS' website for more information on how withdrawals will be taxed.

- Source: MOF

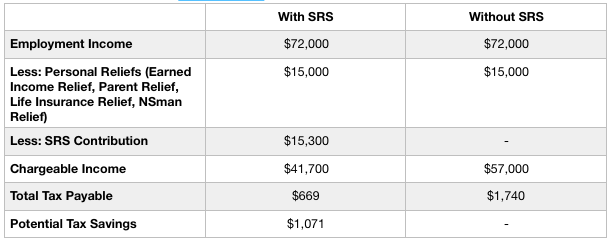

Tax savings… How much can I save?

Here is an illustration for you:

Check out the calculator on IRAS’ website!

Potentially, you have freed up a lot more than the amount of $1,071 just by voluntarily contributing to your SRS account!

The potential tax savings you will enjoy will be in the form of cash and you have $15,300 sitting in the SRS account earning 0.05% p.a* interest, and not forgetting tax savings on withdrawals!

*The current interest rate on balances in the SRS Account which are not invested is at 0.050% p.a

WAIT... 0.05%pa?!?!

Yes, it is just 0.05%pa if you choose to do nothing with it. In fact, there are many options available for you as follows:

unit trusts

single premium insurance

shares

bonds

fixed deposits (local/foreign currency)

Do you know you enjoy tax-free accumulation of gains on your investments with your SRS monies?

“Investment returns are accumulated tax-free and only 50% of the withdrawals from SRS are taxable at retirement (referred to as a “50% tax concession”). Please refer to IRAS' website for more information on how withdrawals will be taxed.

- Source: MOF

“How can I earn more with my SRS monies?”

Step 1: Contact your financial representatives & open a SRS account

All Singaporeans, Permanent Residents and foreigners welcomed

At least 18 years old

Not an undischarged bankrupt

Do not own a SRS account and have not closed an SRS account before

Step 2: Contact your professionals in the relevant fields (more details here)

unit trusts

single premium insurance

shares

bonds

fixed deposits (local/foreign currency)

Step 3: Continue contributing to your SRS account yearly!

be sure to do it before 31 December yearly!

“Can I withdraw my SRS monies?”

Now, let us recap...

“The SRS is part of the Singapore government’s multi-pronged strategy to address the financial needs of a greying population by helping Singaporeans to save more for their old age.”

- Source: MOF

This actually means that the SRS is devised to help individuals better prepare their retirement with extra savings apart from the CPF monies and one should withdraw SRS monies only after retirement age.

However, there is still flexibility with regards to withdrawals due to any circumstances, before the statutory retirement age of 62.

All individuals wishing to participate in the SRS contribution have to be aware that

100% of the withdrawal amount will be taxed, if you wish to withdraw before the age of 62

A 5% penalty charge will be imposed to your withdrawals before the age of 62 (unless it is made under exceptional circumstances; read more here)

Only 50% of the withdrawal amount will be taxable, if the withdrawal is after the age of 62

“What is it about the tax-free withdrawals then?”

Assuming that you currently have got $400,000 at the age of 62 and you are retired and do not have a main source of income.

The SRS scheme allows individuals to enjoy the tax-free withdrawals over a period of 10 years from your first withdrawal upon the age of 62.

And accordingly, 50% of the withdrawals are taxable but the Resident Tax Rate for the first $20,000 of your income is at zero…

So this goes on until the 10th year upon your first withdrawal of your SRS monies.

And viola! you have potentially enjoyed tax savings upon your withdrawals, for a good 10 years!

“Everything sounds so nice.. I am sure there are some down-sides to this”

Indeed! 100% of the withdrawal amount will be taxed, after the 10 years of tax-free withdrawals.

And in fact, this is considered as a happy problem because you still have sufficient money to aid your retirement!

But do not worry much about the tax payable, as the tax rate you eventually end up paying may most likely be a small percentage.

For example, you have started contributing SRS at a young age and have accumulated $500,000 in your SRS account at the age of 62. You can proceed to withdraw tax-free for the next 10 years and have a remaining amount of $100,000.

You may then plan to withdraw $50,000 yearly for the next two years, the tax payable will be $1,250 per year based on current tax rates. You can do the math yourself!

Remember, the Supplementary Retirement Scheme (SRS) is to complement your CPF retirement funds as well as other retirement plans that you have put in place. Therefore, there is great flexibility in utilising SRS to enjoy tax savings, to earn higher returns, and most importantly to enjoy your retirement!

Like what you read? Share it with your friends!

Comments